Itemized Deductions in 2026: What Retirees Need to Know

The short answer: Three changes from the One Big Beautiful Bill reshape itemizing for retirees. The SALT cap jumps to $40,000 for 2025–2029 (with a phase-out starting at $500,000 MAGI), a new 0.5% AGI floor reduces charitable deductions starting in 2026, and high-income itemizers in the 37% bracket face an additional cap. Non-itemizers also get a new above-the-line charitable deduction starting in 2026. Whether to itemize is now a year-by-year decision — and one that interacts with Roth conversions, QCDs, and IRMAA planning.

Key takeaways

- The SALT cap rose from $10,000 to $40,000 for 2025–2029, phasing down between $500,000 and $600,000 of modified AGI.

- Starting in 2026, charitable deductions are only allowed above 0.5% of AGI, but suspended amounts carry forward five years.

- Non-itemizers can deduct up to $1,000 ($2,000 joint) in cash gifts to charity starting with 2026 returns.

- Qualified Charitable Distributions (QCDs) become even more attractive — they bypass AGI entirely and aren’t subject to the new floor.

- The itemize-vs-standard-deduction decision is no longer set-it-and-forget-it. Run the numbers annually.

Why does itemizing matter again for some retirees?

After the Tax Cuts and Jobs Act, only about 10% of taxpayers itemized. The new SALT cap of $40,000 brings itemizing back into play for many higher-income retirees — especially those in high-tax states like Maryland.

Before 2018, nearly 30% of taxpayers itemized. The TCJA changed that by doubling the standard deduction and capping SALT at $10,000. For retirees with paid-off mortgages and moderate state taxes, the standard deduction simply won.

That math just shifted. In our work with retirees, itemizing tends to make sense again when one or more of the following applies:

- You live in a higher-tax state — Maryland, New Jersey, New York, California, Connecticut — where state income and property taxes together easily exceed $10,000.

- You give substantial amounts to charity, especially if you have a long-standing giving tradition.

- You carry significant mortgage interest, perhaps from a recent refinance or a second home.

- You have unusually large medical expenses (above 7.5% of AGI).

- You’re in a high-income year — perhaps from Roth conversions, large capital gains, or sizable IRA distributions.

For Maryland retirees in particular, the new SALT cap is the most consequential change. A couple paying $18,000 in Maryland state income tax and $12,000 in property tax used to lose two-thirds of that deduction. Under the new rules, they can deduct the full $30,000 — provided their income stays below the phase-out.

How does the new $40,000 SALT cap work?

For tax years 2025–2029, the SALT deduction cap is $40,000 ($20,000 for married filing separately). It phases down by 30 cents per dollar of modified AGI above $500,000 and reverts to $10,000 once MAGI hits $600,000. The cap escalates roughly 1% per year through 2029.

What counts as SALT?

- State and local income taxes (or sales taxes, if you elect that option)

- Real property taxes on your primary residence and any other real estate

- Personal property taxes (such as value-based vehicle registration fees)

A Maryland worked example

Consider a Maryland couple with $180,000 in retirement income, paying $18,000 in Maryland state income tax and $12,000 in property taxes:

- Old rule: $10,000 deductible (out of $30,000 paid)

- New rule: $30,000 deductible — the full amount, since they’re below the phase-out

- Estimated federal tax savings: roughly $4,000–$5,000, depending on their marginal bracket

How the income phase-out works

Here’s where many filers — and even some tax preparers — get tripped up. The $40,000 cap doesn’t apply uniformly. It phases down by 30% of every dollar your modified AGI exceeds $500,000 ($250,000 MFS), but never below the old $10,000 floor.

Example: A married couple with $580,000 in modified AGI and $35,000 in state and local taxes:

- MAGI exceeds the $500,000 threshold by $80,000

- 30% × $80,000 = $24,000 reduction

- Their SALT cap drops to $16,000 ($40,000 – $24,000)

- They deduct $16,000 even though they paid $35,000

Once MAGI reaches $600,000 or higher, the cap reverts entirely to $10,000.

For most retirees, modified AGI equals regular AGI. The MAGI add-backs (foreign earned income exclusion, foreign housing exclusion, certain U.S. territory income) only matter if you have those specific income types.

Why the phase-out matters for retirement planning

The phase-out creates a few planning levers:

- Roth conversion timing. A conversion that pushes MAGI from $480,000 to $560,000 doesn’t just create income tax — it can erase $24,000 of SALT deductions. Model both costs together.

- Income bunching. If your income varies year-to-year (capital gains, business income, large IRA distributions), aim to use the full SALT benefit in lower-income years.

- The 2029 cliff. The enhanced cap currently expires after 2029 unless Congress extends it. If you’re in your early 60s now, this is roughly a five-year window to plan around.

What changes for charitable giving in 2026?

Two things change starting with 2026 returns. Itemizers can only deduct charitable gifts above 0.5% of AGI, with the suspended portion carrying forward up to five years. Non-itemizers gain a new above-the-line deduction of up to $1,000 ($2,000 joint) for cash gifts to qualified public charities.

The 0.5% AGI floor for itemizers

Beginning with 2026 returns (filed in 2027), charitable contributions are only deductible to the extent they exceed 0.5% of AGI. This mirrors the structure already in place for medical expenses, just at a much lower threshold.

Example: A retired couple with $200,000 AGI donates $8,000 to their church and other charities in 2026:

- 0.5% of $200,000 = $1,000 floor

- Deductible amount = $8,000 – $1,000 = $7,000

Any portion below the floor in a given year carries forward up to five years. So a $2,000 gift in a year with a $1,000 floor isn’t lost — the suspended $1,000 can be added to next year’s deductible amount if your giving in 2027 clears that year’s floor.

Why this hits middle-income givers hardest

For a widow with $85,000 in retirement income who gives $3,000 per year:

- Floor = $425

- Deductible = $2,575

- Lost deduction = $425 per year, or roughly $100 in additional tax

Over a decade of consistent giving, that adds up. The bigger concern is behavioral — modest givers who used to feel rewarded for their generosity may now feel a small tax penalty, particularly if their itemizing benefit was already marginal.

The non-itemizer charitable deduction

Congress balanced the scales somewhat. Starting in 2026, non-itemizers can deduct up to $1,000 ($2,000 joint) in cash gifts to charity, directly reducing AGI. No Schedule A required.

Important restrictions:

- Cash only — no donated goods, no appreciated securities.

- Gifts must go to qualified public charities, not private foundations or donor-advised funds.

- Substantiation rules still apply (bank records or written acknowledgments).

Why Qualified Charitable Distributions (QCDs) become more valuable

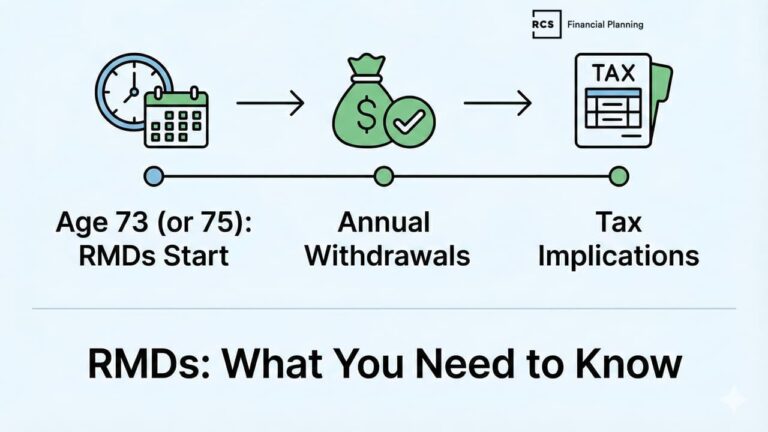

If you’re 70½ or older, you can donate directly from your IRA to qualified charity. For 2026, the annual QCD limit is $111,000 per person. These distributions:

- Count toward your required minimum distribution

- Are excluded from taxable income entirely

- Aren’t subject to the new 0.5% floor — because they never hit AGI

- Reduce IRMAA exposure

- Work whether you itemize or not

For most retirees with IRA assets, QCDs are now clearly the most tax-efficient way to give. Yet we routinely see clients write December checks to charity without considering this option first.

Should you bunch contributions?

If your annual giving sits near or below the 0.5% floor, you have two options worth modeling with your advisor:

- Bunch into a donor-advised fund in a high-income year, claim the full itemized deduction, then grant to charities over multiple years.

- Alternate years — itemize and give heavily in one year, take the standard deduction (and use the new $1,000/$2,000 above-the-line cash deduction) in the next.

The Essential Retirement Readiness Checkup

See how seven critical retirement decisions interact to shape your income, taxes, and long-term security — often in ways most people don’t see until it’s too late. Get clarity on how your retirement decisions work together — not just on paper, but in real life.

How does the new high-income deduction limit work?

Starting with 2026 returns, taxpayers in the 37% federal bracket have their itemized deductions reduced by 2/37 of the lesser of (a) total itemized deductions or (b) the amount their taxable income exceeds the 37% threshold. The practical effect is to cap the tax benefit of itemizing at roughly 35% rather than 37%.

The 2/37 reduction explained

For 2025, the 37% bracket begins at taxable income above $626,350 (MFJ) or $313,175 (single). These thresholds adjust annually.

Example: A married couple with $726,350 in taxable income and $50,000 in itemized deductions:

- Taxable income exceeds the 37% threshold by $100,000

- The lesser of itemized deductions ($50,000) or excess income ($100,000) = $50,000

- Reduction = 2/37 × $50,000 = $2,703

- Allowed itemized deductions = $47,297

The effective haircut runs about 2%–6% of itemized deductions for most affected retirees — meaningful, but smaller than the SALT phase-out for many.

Who actually feels this?

- Successful business owners or executives in early retirement still earning substantial income

- Retirees with large investment income in capital gain years

- Anyone taking very large IRA distributions (voluntary or required)

- Non-spouse beneficiaries draining inherited retirement accounts under the 10-year rule

Planning levers for high-income retirees

- QCDs reduce AGI, which can help you stay below the 37% threshold entirely.

- Tax-free income sources (Roth distributions, municipal bond interest) don’t count toward the threshold.

- Multi-year bracket modeling sometimes favors taking a large distribution in one year rather than spreading evenly — if the alternative pushes you into the 37% bracket every year.

- Bunching deductible expenses into below-threshold years preserves their full value.

Should you still itemize? A retiree’s decision framework

Compare your projected itemized deductions (SALT capped per the phase-out, charitable above the 0.5% floor, mortgage interest, and medical above 7.5% of AGI) against your standard deduction including the age 65+ addition. Re-run the comparison every year — life and tax law both change.

The age 65+ standard deduction sets a high bar

For 2026, the standard deduction is $16,100 single / $32,200 MFJ. Add the age 65+ additions of $2,050 (single) or $1,650 per qualifying spouse (MFJ), and a married couple both 65+ is working against a $35,500 standard deduction.

That’s a high bar — particularly with the new charitable floor pulling itemized deductions down and the high-income reduction shaving the top.

Annual checklist

- Estimate your AGI (wages, retirement distributions, taxable Social Security, investment income).

- Calculate your standard deduction including 65+ additions.

- Total your potentially deductible expenses by category.

- Apply the new rules — SALT cap and phase-out, 0.5% charitable floor, 37% bracket reduction.

- Compare. Decide.

- Consider timing moves — bunch, defer, or accelerate based on the comparison.

What are the most common itemizing mistakes retirees make?

The five most common errors we see are assuming last year’s approach still works, poor charitable recordkeeping, ignoring state conformity, making year-end cash gifts when a QCD would be better, and treating itemizing as separate from overall retirement income planning.

- Assuming last year’s approach works this year. Tax law and your own income mix both change. What worked at 62 often doesn’t work at 73 once RMDs begin.

- Sloppy charitable recordkeeping. With new carry-forward rules, undocumented gifts can cost real money over several years.

- Ignoring state conformity. Maryland and many other states have their own itemizing rules. You may itemize for federal but take the standard deduction for state — or vice versa.

- Cash gifts when a QCD would be better. If you’re over 70½, the December cash gift is almost always the inferior choice.

- Treating itemizing in isolation. Roth conversions, Social Security timing, IRMAA, and withdrawal sequencing all interact with the itemize-vs-standard-deduction call.

How does itemizing fit into broader retirement tax planning?

Good retirement tax planning is about minimizing lifetime tax — not maximizing this year’s deductions. Your itemizing approach should coordinate with income sequencing, Roth conversion strategy, Social Security timing, IRMAA management, and required minimum distributions.

Five interactions worth modeling explicitly:

- Income sequencing. The order in which you draw from taxable, tax-deferred, and tax-free accounts drives your AGI — which in turn drives SALT phase-outs, the charitable floor, and the high-income reduction.

- Roth conversion planning. Converting in a year that pushes you over $500,000 MAGI costs you more than just the income tax on the conversion.

- Social Security timing. Delaying benefits often means higher income later, which can shift your itemizing math.

- IRMAA. Modified AGI from two years ago drives Medicare Part B and D premiums. Sometimes managing AGI for IRMAA matters more than maximizing one year’s deductions.

- RMDs. Once distributions are required, you have less control over your income. Plan your itemizing approach before RMDs begin.

What should you do next?

If your 2025 income could approach the SALT phase-out, model it before year-end planning. If you’re over 70½ and giving to charity, look at QCDs before writing your next check. If 2026 is shaping up to be a Roth conversion year, coordinate the conversion size with the SALT phase-out math.

For most retirees, the practical work falls into three buckets:

- For your 2025 return: confirm whether the new $40,000 SALT cap meaningfully changes your itemize-vs-standard call. If you’re near the phase-out, run the numbers carefully.

- For 2026 planning: decide whether to bunch charitable gifts, use QCDs, or rely on the new non-itemizer deduction.

- For the 2026–2029 window: coordinate the enhanced SALT cap with Roth conversion, Social Security, and RMD planning before the rules potentially revert.

Want a second set of eyes on your retirement tax strategy? Schedule a complimentary introductory call → to talk through whether itemizing still fits your situation, how to structure charitable giving more tax-efficiently, and how these rules connect to the rest of your retirement income plan.

Not ready to talk? Download our free retirement checklists → to take stock of where you stand.

Itemized Deductions FAQ

Ready for clarity and confidence in your retirement plan?

This material is provided for educational, general information, and illustration purposes only. You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. Nothing contained in the material constitutes tax advice, a recommendation for the purchase or sale of any security, or investment advisory services. This content is published by an SEC-registered investment adviser (RIA) and is intended to comply with Rule 206(4)-1 under the Investment Advisers Act of 1940. No statement in this article should be construed as an offer to buy or sell any security or digital asset. Past performance is not indicative of future results.