Inherited IRA RMD Rules: Are You Making a Tax Mistake That Could Cost Thousands?

You’ve inherited an IRA. Great – but do you really know what the IRS expects from you?

Most people assume they can leave the account untouched or withdraw as needed. But what if your strategy accidentally triggers penalties or taxes that drain your inheritance faster than you ever imagined?

In this article, we’ll unpack the often-confusing required minimum distribution (RMD) rules for inherited IRAs, especially after the SECURE Act. Whether you’re a spouse, child, or non-family beneficiary, the choices you make today can impact your tax bill for years to come.

Understanding Inherited IRA RMD Rules

What Is an Inherited IRA?

An inherited IRA is exactly what it sounds like: an IRA you receive upon someone’s death. But unlike a regular IRA, you can’t contribute to it – and the IRS has strict rules on how and when you must take money out.

👉 Spouse vs. Non-Spouse Beneficiaries

- Spouse beneficiaries have more flexible options, including treating the account as their own.

- Non-spouse beneficiaries must follow distribution rules based on their relationship to the original owner.

Why Did RMD Rules Change Under the SECURE Act?

Before 2020, non-spouse beneficiaries could “stretch” distributions over their lifetime, minimizing annual taxes.

But with the SECURE Act (2019), Congress ended this strategy for most. Now, non-spouse beneficiaries must deplete the account within 10 years, fundamentally changing the tax planning landscape.

Key SECURE Act Changes

| Before SECURE Act | After SECURE Act (2020 onwards) |

|---|---|

| Non-spouse beneficiaries could stretch RMDs over their life expectancy. | Non-spouse beneficiaries must withdraw the entire account within 10 years (with limited exceptions). |

Who Needs to Take RMDs and When?

Spouse Beneficiaries

Spouses have unique options:

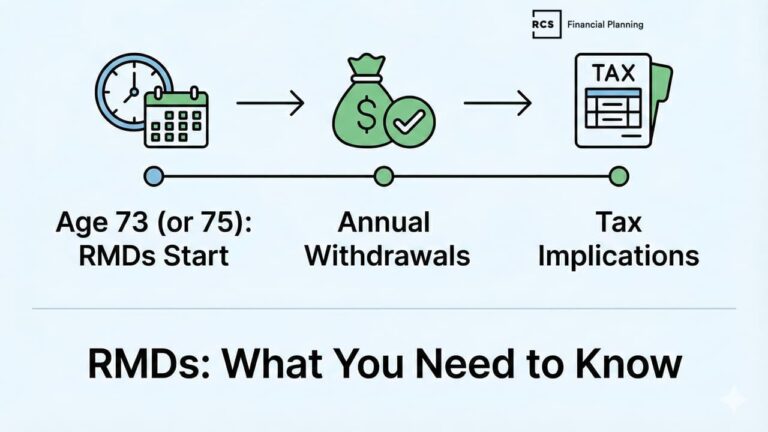

- Treat as Own IRA – Roll over into their own IRA and delay RMDs until age 73 (or 75, depending on birth year).

- Remain as Beneficiary IRA – Keep as an inherited IRA and take RMDs based on their life expectancy.

👉 Why This Matters: Choosing the wrong option could trigger unnecessary distributions and taxes earlier than required.

Non-Spouse Beneficiaries

The 10-Year Rule

If you’re a non-spouse beneficiary, you generally must fully withdraw the account within 10 years of the original owner’s death.

✅ Important Caveat: Starting in 2025, annual RMDs are required for NEDBs if the decedent died after their RBD, in addition to the account needing full depletion by year 10.

Eligible Designated Beneficiaries (EDBs)

Certain beneficiaries can still use the lifetime stretch:

- Surviving spouse

- Minor children (until age of majority – which is age 21, NOT your state’s age of majority)

- Disabled individuals

- Chronically ill individuals

- Individuals <10 years younger than the decedent

👉 Example: A child with disabilities can stretch distributions over their lifetime, reducing annual tax burdens.

Non-Designated Beneficiaries

These include:

- Estates

- Charities

- Certain trusts

Distribution Rules:

- If the owner died before RMD age: Entire account must be distributed within 5 years.

- If the owner died after RMD age: Distributions continue over the decedent’s remaining life expectancy.

Not sure if you’re missing something in your retirement plan?

When you claim Social Security affects your taxes. Your tax bracket affects your Medicare premiums. Your withdrawal strategy affects all of it. This free guide shows you how seven retirement decisions connect — and why they can’t be made in isolation.

Calculating RMDs for Inherited IRAs

How to Calculate Your RMD

Use the IRS Single Life Expectancy Table:

- Determine your age in the year after inheritance.

- Find your life expectancy factor.

- Divide the prior year-end account balance by this factor.

Example Calculation

- Beneficiary Age: 50

- Factor: 34.2

- IRA Balance: $300,000

RMD = $300,000 ÷ 34.2 = $8,772

Source: IRS Publication 590-B

Common Mistakes

❌ Failing to take annual RMDs if required.

❌ Waiting until year 10 to withdraw the full amount, triggering massive tax spikes.

❌ Misunderstanding rules for inherited Roth IRAs, assuming RMDs are required.

Penalty Alert

Missing an RMD triggers a 25% excise tax penalty, reduced to 10% if corrected promptly (SECURE Act 2.0).

Special Considerations for Inherited Roth IRAs

Non-spouse beneficiaries of inherited Roth IRAs do not have annual RMDs but must fully distribute by December 31 of the 10th year after death. Distributions remain tax-free if the Roth has been open 5+ years.

Planning Strategies to Minimize Taxes

1. Spread Withdrawals Over 10 Years

Most beneficiaries wait until year 10 and face a massive tax bill. Strategic annual withdrawals can:

- Keep you in a lower tax bracket.

- Reduce Medicare IRMAA surcharges.

- Minimize Social Security taxation.

👉 Have you considered how these withdrawals impact your overall retirement income plan?

2. Roth Conversions Before Death

For original IRA owners, converting to a Roth before death can:

- Avoid forcing heirs to take taxable distributions.

- Leave a tax-free inheritance, though heirs still must distribute within 10 years.

3. Trust Beneficiaries – Proceed with Caution

The SECURE Act has complicated trust planning:

- Conduit trusts pass RMDs directly to beneficiaries annually.

- Accumulation trusts retain distributions, but funds are taxed at trust tax rates (37% on income over $15,200 in 2025).

👉 Many existing estate plans need updating to align with current law.

Real-Life Scenario: Ignoring RMD Rules Can Be Costly

John inherited his uncle’s $400,000 IRA at age 55.

He decided to wait until year 10 to withdraw the full amount. That year, he earned $150,000 from his job. Adding a $400,000 distribution pushed him into the highest tax bracket, costing him over $120,000 in taxes that could have been avoided with strategic annual withdrawals.

👉 What if your current plan is setting you up for the same painful tax surprise?

Conclusion

Inherited IRA rules aren’t just bureaucratic red tape – they’re a financial minefield. Most people assume they’re handling these accounts correctly, but the reality is far more complex and unforgiving.

Have you considered whether your inherited IRA strategy is optimized for tax efficiency? Or will your decisions cost you – and your family – more than you realize?

Key Takeaways

- Inherited IRA rules changed under the SECURE Act.

- Non-spouse beneficiaries generally must deplete the account within 10 years.

- Missing RMDs can trigger hefty penalties.

- Spouse beneficiaries have flexible options requiring careful evaluation.

- Strategic withdrawals and planning can save thousands in taxes.

Ready for clarity and confidence in your Retirement plan?

30 minutes · No cost · No obligation

This material is provided for educational, general information, and illustration purposes only. You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. Nothing contained in the material constitutes tax advice, a recommendation for the purchase or sale of any security, or investment advisory services. This content is published by an SEC-registered investment adviser (RIA) and is intended to comply with Rule 206(4)-1 under the Investment Advisers Act of 1940. No statement in this article should be construed as an offer to buy or sell any security or digital asset. Past performance is not indicative of future results.